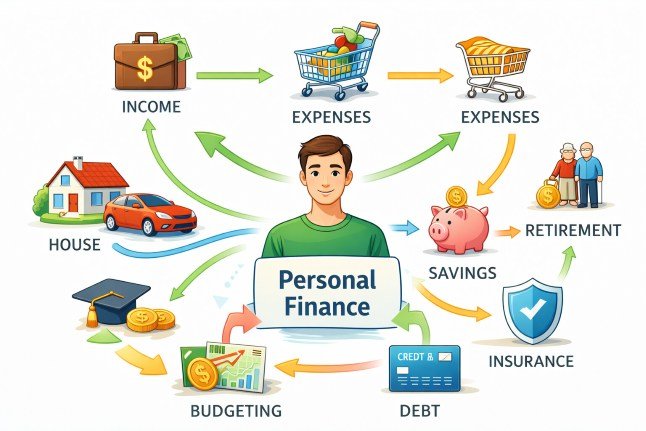

Personal Finance: The Complete Guide to Managing Money

Personal Finance: The Complete Guide to Managing Money

How to Create a Personal Budget That Works

How to Create a Personal Budget That Works

Emergency Funds Guide 2026

Emergency Funds Guide 2026

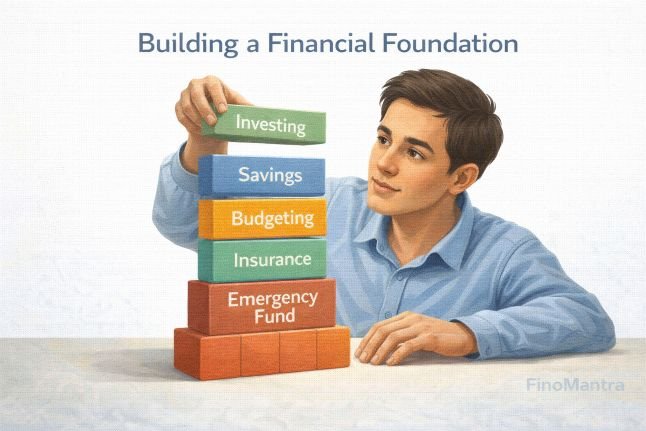

Financial Planning for Young Adults

Financial Planning for Young Adults

How to Set Financial Goals & Stick to Them

How to Set Financial Goals & Stick to Them

3 Best Budgeting Methods in 2026: 50/30/20 vs ZBB vs Envelope

3 Best Budgeting Methods in 2026: 50/30/20 vs ZBB vs Envelope