Bonds: A Complete Professional Guide to Bond Investing

Bonds: A Complete Professional Guide to Bond Investing

Government Bonds vs Corporate Bonds: Differences, Pros & Cons

Government Bonds vs Corporate Bonds: Differences, Pros & Cons

Bond Laddering Strategy

Bond Laddering Strategy

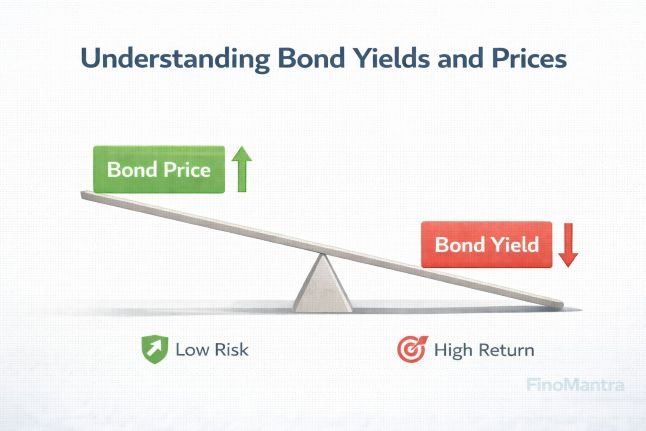

Understanding Bond Yields and Prices

Understanding Bond Yields and Prices

What Are Risk-Free Bonds?

What Are Risk-Free Bonds?

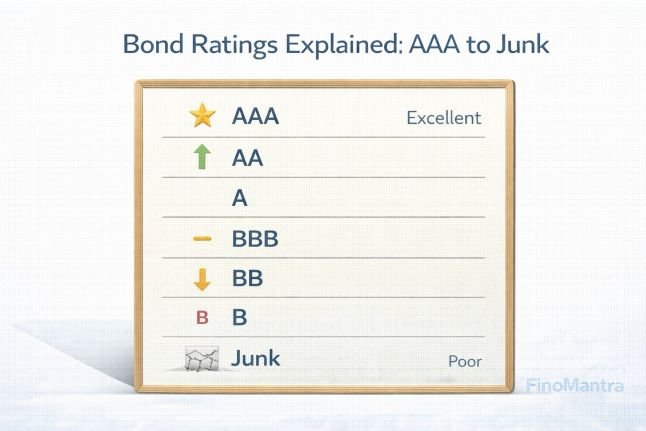

Bond Ratings

Bond Ratings